What Is Important to Know About Life Insurance with Savings (Endowment Life Insurance)?

Life insurance with savings is an important financial tool for those who aim not only to provide financial protection for their loved ones in the event of unforeseen circumstances but also to accumulate capital for the future.

The essence of endowment life insurance lies in the long-term accumulation of funds to build capital for future needs—such as creating a financial cushion for retirement, saving for children's education, purchasing a first home, starting a business, and more.

While accumulating funds, the client also ensures financial protection for their loved ones in case of death: the beneficiaries will receive the full amount planned to be accumulated over the policy term. Additionally, coverage for accidents, disability, critical illnesses, and similar risks can be included.

A key advantage of endowment life insurance is that it is the only type of insurance in Ukraine that allows policyholders to receive an annual tax rebate from the state—up to 18% of the insurance premium paid.

Additional Investment Income (AII)

One of the key components of life insurance is the **Additional Investment Income (AII)**, which can significantly increase the overall value of the insurance policy. This is because the insurance reserves formed from client payments do not simply sit idle within the company—they are invested in reliable financial instruments.

The main goal of these investments is to generate additional income, which can then be used to increase the amount payable to the client either in the event of an insured event or at the end of the policy term. This additional income is a crucial factor that makes endowment life insurance more attractive compared to traditional savings or deposit programs.

The Additional Investment Income (AII) is credited to each client based on the amount of premiums paid, the policy term, and the currency of the contract. Compound interest is applied, meaning AII is calculated not only on the original contributions but also on the income accrued in previous years.

The results of the insurance company’s investment activities are approved annually.

Investment Policy of UNIQA Ukraine

The investment activities of life insurance companies are regulated by the current legislation of Ukraine. According to these legal requirements, insurance reserve funds must be allocated with consideration for **safety, profitability, liquidity, and diversification**, and may be represented by assets in the following categories:

- Funds in current (bank) accounts

- Bank deposits

- Foreign currency deposits in accordance with the insurance policy currency

- Real estate

- Securities

- Government-issued securities

- Reinsurance receivables

- Long-term financing (lending) of residential construction

- Investments in the Ukrainian economy

- Banking metals (precious metals)

- Policyholder loans to individuals

A cautious and balanced investment policy is the key to preserving and growing our clients’ funds. The client is always at the center of our focus, and the investment policy of UNIQA Ukraine is aimed at ensuring the highest level of reliability for our clients’ investments.

Insurance reserves are placed in full compliance with legal requirements, but exclusively in low-risk assets. As of the end of 2023, the reserves were allocated as follows:

- Bank deposits in institutions owned by major international financial corporations with the highest reliability ratings, and in state-owned banks – 6% of total insurance reserves

- Current account funds in banks with the same high reliability and ownership structure – 2% of total insurance reserves

- Ukrainian government bonds – 92% of insurance reserves

It is important to note that the insurance company guarantees a minimum level of return, regardless of investment performance. This provides clients with additional security and reduces the risk of financial loss, especially during economically unstable periods.

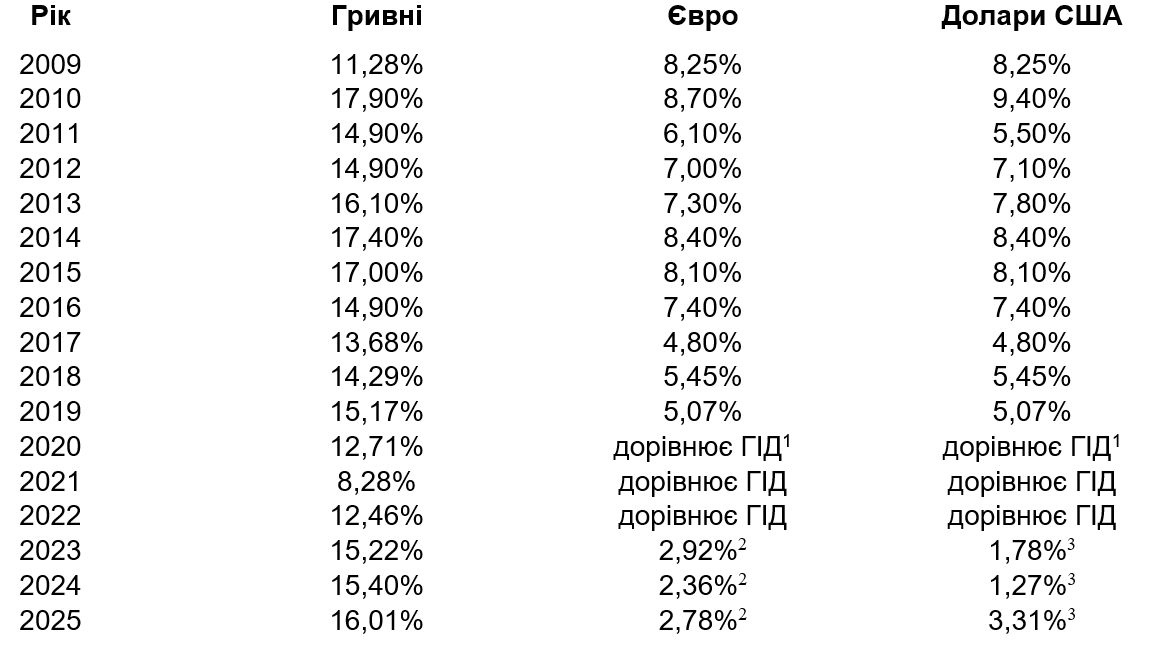

Investment Performance of the Company by Year

¹Guaranteed investment income (GII) — the guaranteed return specified in the insurance contract

²For contracts with GII of 0.5% and 2%. For others — within the guaranteed return

³For contracts with GII of 0.5%. For others — within the guaranteed return